by Lee & Associates

While continuous improvement is needed, the economy is recovering from the COVID-19 pandemic. 2022 will build on the recovery that is already underway both in the macroeconomy and in commercial real estate markets. However, don’t expect commercial real estate markets or the rest of the economy to go back to exactly as things were before the pandemic. The pandemic was more than just a shock to aggregate demand. It changed the way people live, shop, and conduct business. Some of the changes may dissipate over time, while others are likely to be permanent. Nearly every commercial real estate sector has been and will continue to be affected one way or another. This report will explain what trends to expect and watch for in 2022. Since no forecast is infallible, keep in mind that there are both upside and downside risks to the outlook. Here are the top seven things you need to know for 2022:

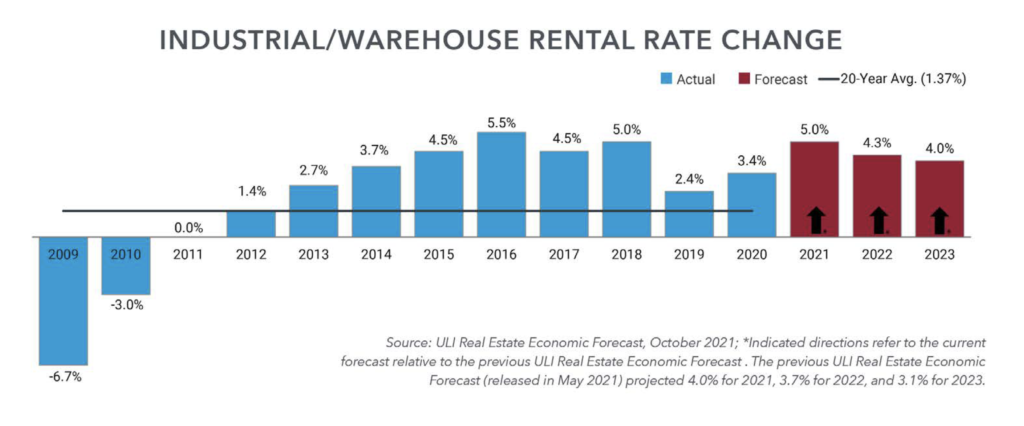

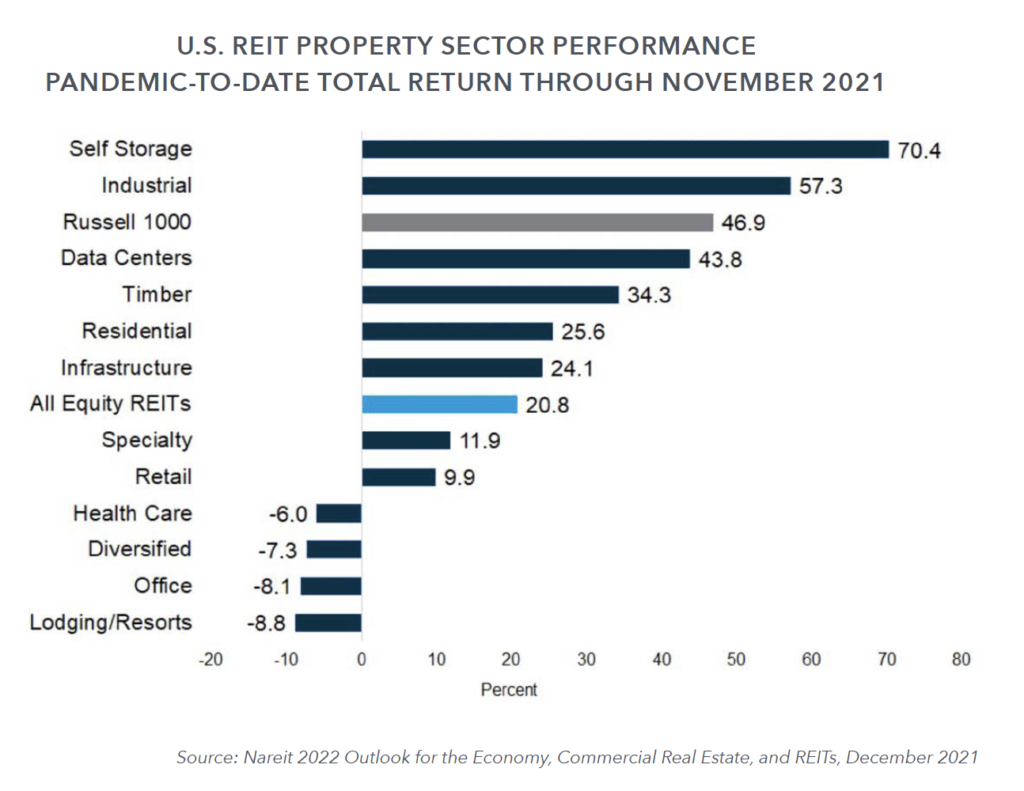

THE INDUSTRIAL SECTOR, INDUSTRIAL REITS, AND DATA CENTERS WILL CONTINUE TO GROW IN 2022.

The pandemic’s further entrenchment of e-commerce into American life has been an enormous lift for industrial and logistics real estate. This year, U.S. e-commerce sales will make up about 14.5% of total retail sales, or $709.78 billion. By the end of 2024, that percentage will grow to 18.1% of all retail sales, with online sales surpassing $1 trillion for the first time. Consequently, U.S. demand for industrial real estate could reach an additional 1 billion square feet by 2025.1 For that reason, rent growth for the sector is expected to continue above the long-term average not only for 2022 but for the foreseeable future.2

Digital communications provided a lifeline during the pandemic, from online conference meetings for work to e-commerce purchases by consumers and streaming movies online for entertainment. The use of these conveniences has continued to rise even as the economy reopens, generating robust demand for digital real estate sectors like data centers, infrastructure/cell towers, and industrial/logistics facilities.

THE OFFICE SECTOR IS NOT DEAD. IT WILL REMAIN THE HUB OF BUSINESS, BUT HYBRID SCHEDULES THAT ALLOW FOR FLEXIBLE WORK-FROM-HOME OPPORTUNITIES ARE HERE TO STAY.

According to the Labor Department’s monthly employment report, millions of employees are returning to the office each month, yet many employers are embracing a flexible work-from-home model.

The critical development to watch is not how many employees commute each month. Instead, keep an eye on the peak space needs for the days when all employees are in the office for teamwork and communication, as this will drive overall demand for office space. In addition, watch whether employers redesign the office space to eliminate individual offices and workstations or decrease density within the office on the days employees work from home.3

EXPECT ANOTHER STRONG YEAR FOR THE MULTIFAMILY AND HOUSING SECTOR.

The multifamily and housing sector is radically undersupplied while demand for both is at all-time highs. Expect rents and home prices to remain high; however, the rate of appreciation will be limited by issues related to affordability.

The markets for apartment rentals and home purchases usually move in opposite directions, with a strong housing market generally accompanied by soft rental markets and vice versa. During the pandemic, however, the desire for more living space while working and studying from home has driven rental and ownership markets to record highs. As a result, apartment properties rose at a double-digit rate through the third quarter of 2021.4

DEMOGRAPHIC SHIFTS WILL ACCELERATE THE DEMAND FOR SENIOR LIVING FACILITIES AND ELDER CARE SERVICES.

COVID-19 infections negatively affected many residential health care facilities, including senior living and skilled nursing, limiting move-ins and causing a sharp drop in occupancy rates. Occupancy began to rise again in the second half of 2021, but remains several percentage points below pre-pandemic levels.

Progress against the pandemic, and the high vaccination rates among those 65 and older, will drive further recovery in senior housing and skilled nursing in 2022. Full recovery, however, will not occur until 2023. In addition, the demographic wave of Baby Boomers will fuel longer-term demand.

EXPECT ANOTHER BANNER YEAR FOR THE SELF-STORAGE SECTOR.

The self-storage sector has been a star performer during the pandemic as strong housing markets and home purchases have spurred demand for storage. Using one metric to demonstrate their success, U.S. self-storage REITs outperformed all other sectors and indices.

EVEN THOUGH INFLATION WILL BE HIGH FOR THE FIRST HALF OF THE YEAR, EXPECT IT TO GRADUALLY DECREASE AS THE YEAR PROGRESSES. THE U.S. IS NOT CURRENTLY GOING THROUGH A 70’S STYLE STAGFLATION.

The Federal Reserve will likely begin slow, small increases in its target for short-term interest rates in the latter half of 2022. Long-term interest rates will remain low providing attractive financing conditions for commercial real estate.

The 12-month change in CPI has risen to a 30-year high, but this time frame misses the large swings that took place over shorter periods during the pandemic. Core CPI inflation on a 3-month annualized change surged above 10% in June as supply chain problems intensified, but has subsequently slowed to 3%-4%.

The supply chain bottlenecks aren’t going away quickly, however, and shortages in critical goods and commodities will continue to fuel price pressures in the medium term—but in the longer term, inflation rates are likely to cool.5

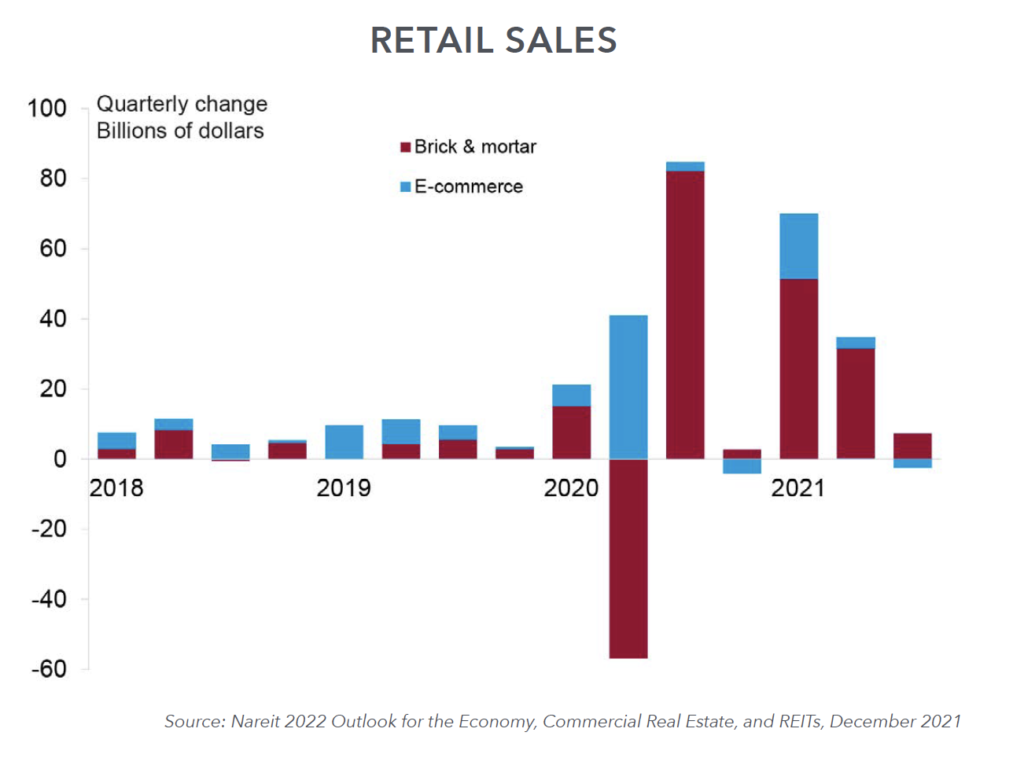

EXPECT REDUCTIONS IN RETAIL VACANCIES AS TENANTS CONTINUE TO LEASE BRICK-AND MORTAR RETAIL PROPERTY.

Contrary to a widespread misperception, retail is not dead. E-commerce consumption accelerated dramatically during the early months of the pandemic, while sales through brick-and-mortar channels declined as social distancing requirements were put in place. After that, however, in store sales rebounded to above pre-pandemic levels as many consumers still prefer shopping in person for items where size, fit, and appearance are essential. Over the past year, online and in-store sales have both risen.

Brick-and-mortar sales came back with a vengeance in 2021 as stores reopened, more than reversing their earlier decline in 2020 with an $82 billion gain in the third quarter of 2021. What is most surprising, though, is that e-commerce sales didn’t fall with the rebound in brick-and-mortar sales, but instead have continued to build on their earlier increases.

Consumers have demonstrated that they still appreciate in-store shopping for specific items, even as they prefer the convenience of online purchases for others. In particular, shoppers often want to check the size and fit and appearance for clothing, shoes, and other fashion items, or they may simply enjoy visiting shops and seeing the displays as a break from mouse clicks online.6

Sources:

1 Prologis: https://bit.ly/3qPPaze and https://bit.ly/3sY9xwJ

2 ULI Forecast

3 Forbes: https://bit.ly/3HzgyrF

4 Costar Commercial Repeat Sales Indices: https://bit.ly/3eIDzw4

5 Economist Calvin Schnure: https://bit.ly/3HzgyrF and Bloomberg: https://bloom.bg/3mR5rmg

6 NAREIT: https://bit.ly/32E2qin

The information and details contained herein have been obtained from third-party sources believed to be reliable, however, Lee & Associates has not independently verified its accuracy. Lee & Associates makes no representations, guarantees, or express or implied warranties of any kind regarding the accuracy or completeness of the information and details provided herein, including but not limited to, the implied warranty of suitability and fitness for a particular purpose. Interested parties should perform their own due diligence regarding the accuracy of the information. The information provided herein, including any sale or lease terms, is being provided subject to errors, omissions, changes of price or conditions, prior sale or lease, and withdrawal without notice. Third-party data sources: The sources listed above, CoStar Group, Inc., and Lee & Associates proprietary data. Copyright 2022 Lee & Associates all rights reserved.